Coinsurance clause is used in many forms of insurance for two main reasons; to discourage insureds from using benefits unnecessarily, and to ensure property owners purchase sufficient amount of insurance.

Coinsurance clause is used in many forms of insurance for two main reasons; to discourage insureds from using benefits unnecessarily, and to ensure property owners purchase sufficient amount of insurance.

In health insurance, coinsurance is presented either as a fixed dollar amount per doctor’s visit (in the form of co-pays), a percentage of the total cost of medical care, or a combination of both. As part of risk assessment analysis, in addition to various perils, insurers are faced with “morale hazard”. Morale hazard is defined as an insured’s casual carelessness and indifference towards loss because he has insurance. If the insured bears a portion of the cost, he would reconsider if a doctor’s visit or a medical test is absolutely necessary.

In property insurance, it is used to ensure property owners purchase sufficient amount of coverage.

The rationale for enforcing co-insurance clause comes out of the fact that most accidents result in losses that are partial. As a result, some property owners have a tendency to carry less insurance than the true value of the property being insured, counting on the fact that any loss would be brought under control before the entire property is destroyed, while more prudent property owners would carry sufficient coverage that are more closely indicative of the value of the property at risk. Different insureds would then be paying different premiums on identical properties, thereby contributing unfairly to the pool of premiums from which all losses are paid.

Thus, assume that of two property owners, each carrying inventory worth $300,000, owner number 1 insured his inventory for $240,000; owner number 2 chose to carry only $120,000 of insurance. They each sustained a $60,000 loss. Since the amount of loss is within the coverage amount, they would be fully covered for the loss, although owner number 1 had been paying twice the premium of owner 2.

To distribute the cost of insurance more evenly among all the insureds, many policies contain a clause under which a policyholder agrees to purchase coverage of not less than a certain percentage of the actual value of the property at the time when the loss occurs.

The most commonly used coinsurance percentage is 80%, although other percentages are also available.

So, with a policy containing an 80% coinsurance clause, the policyholder agrees to purchase insurance of not less than 80% of the actual value (or replacement cost) of the property at the time the loss occurs. If the policyholder maintains less than this agreed percentage of coverage, the policyholder will not be entitled to collect in full in case of a loss, but will have to bear part of it. In essence, the policyholder is co-insuring the property together with the insurance company. The insurer will pay only for such percentage of the loss as the amount of insurance in relation to 80% of the actual value of the property at the time of loss. The percentage of loss for which the insurer will pay under these circumstances may be expressed by the formula:

P x L = A

M

Where P is the amount of insurance Purchased, M is the Minimum amount of insurance required – the minimum percentage of the actual value of the property at the time of the loss, L is the amount of the Loss, A is the amount for which the company is liable.

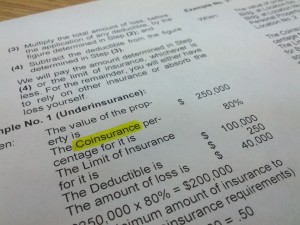

EXAMPLE: Assume a store owner has $100,000 worth of property. He purchased $40,000 coverage in an insurance policy which contains an 80% coinsurance clause. The store suffers a $10,000 loss. The insurer is liable only for one-half of the loss, as follows:

P = amount of insurance purchased $40,000

M = amount of insurance required = $80,000

L = amount of loss = $10,000

Amount insurance company liable for is $5,000 = ½ of the loss

Now further assume a separate store owner who complied with the 80% Coinsurance clause in his policy and insured his stock of $100,000 under a policy of $80,000. Again assuming a $40,000 loss, the loss would be settled in full, as follows:

P = Amount of Insurance Carried = $80,000

M = Amount of Insurance Required = $80,000

L = Amount of Loss = $10,000

Amount insurer liable for is $10,000, 100% of Loss

In practice, in most cases, the actual appraisals of the property are not made when the policy is purchased. The burden falls on the policyholder to estimate the value of the property being insured. The expenses of an actual appraisal are usually saved for large, high-value properties. The Coinsurance clause accounts for the actual cash value of the property at the time of the loss. It is not as important that the coverage amount was sufficient when the policyholder initially purchased the insurance as it is when the loss occurs. If the value of the property has increased, it is the policyholder’s responsibility to increase the coverage amount to stay in compliance with the stipulations of the Co-insurance clause, and to avoid being a co-insurer of his own property.

The effect of the Coinsurance clause on a policyholder’s recovery will be the same whether he purchases one or more policies on the property. Each policy will pay only in the proportion that the amount of insurance in the policy bears to the percentage stated of the actual value of the property. Thus, in the first illustration used above, where the policyholder’s property was worth $100,000, if he carried two policies on the property of $20,000 each, each policy would be liable for 25% of any loss ($20,000 of insurance carried divided by the $80,000 that should have been purchased). Both policies together will be liable for 1/2 of any loss, the same result as when there was only one policy of $40,000.

It is important to keep in mind that the policyholder can never collect more than the amount of coverage he purchased. Therefore, in the first example above, where the policyholder purchased $40,000 of insurance on stock worth $100,000 at the time of the loss, and suffered a total loss of $100,000, he would collect no more than $40,000, the amount he purchased. If the loss is partial, the policyholder would only 40% of the actual loss, since he only carried 40% of the actual worth of the stock. If the policyholder is in compliance with the 80% co-insurance clause and carried $80,000 of coverage at the time the loss occurred, the maximum he can collect is $80,000, the amount he purchased, not the $100,000 worth of inventory.

The Coinsurance clause is merely the minimum amount of insurance which the policyholder must carry in order to collect losses in full, up to the face amount of the policy. Coinsurance clause does not limit the amount of insurance one may purchase. Any property owner may elect to carry insurance of 100% of the value of his inventory. In the event of a total loss, the property owner will be entitled to collect 100% of the policy.